The ability to make direct investments can be very attractive to family members and those running family office investment portfolios. It can mean investing in areas related to the wealth-creating activities of the family members, or areas in which they have developed a particular interest. Many family offices pursue direct investments with a goal of enhanced returns by avoiding the management fees and carried interest of fund investments, in addition to supporting the family’s interest in having more influence, transparency or control in its investments, including pursuit of certain industries and company types. However, directs can be complex, illiquid, risky single-asset investments, with no guarantee of outperformance over funds or publics, and require skilled investment management resources for success.

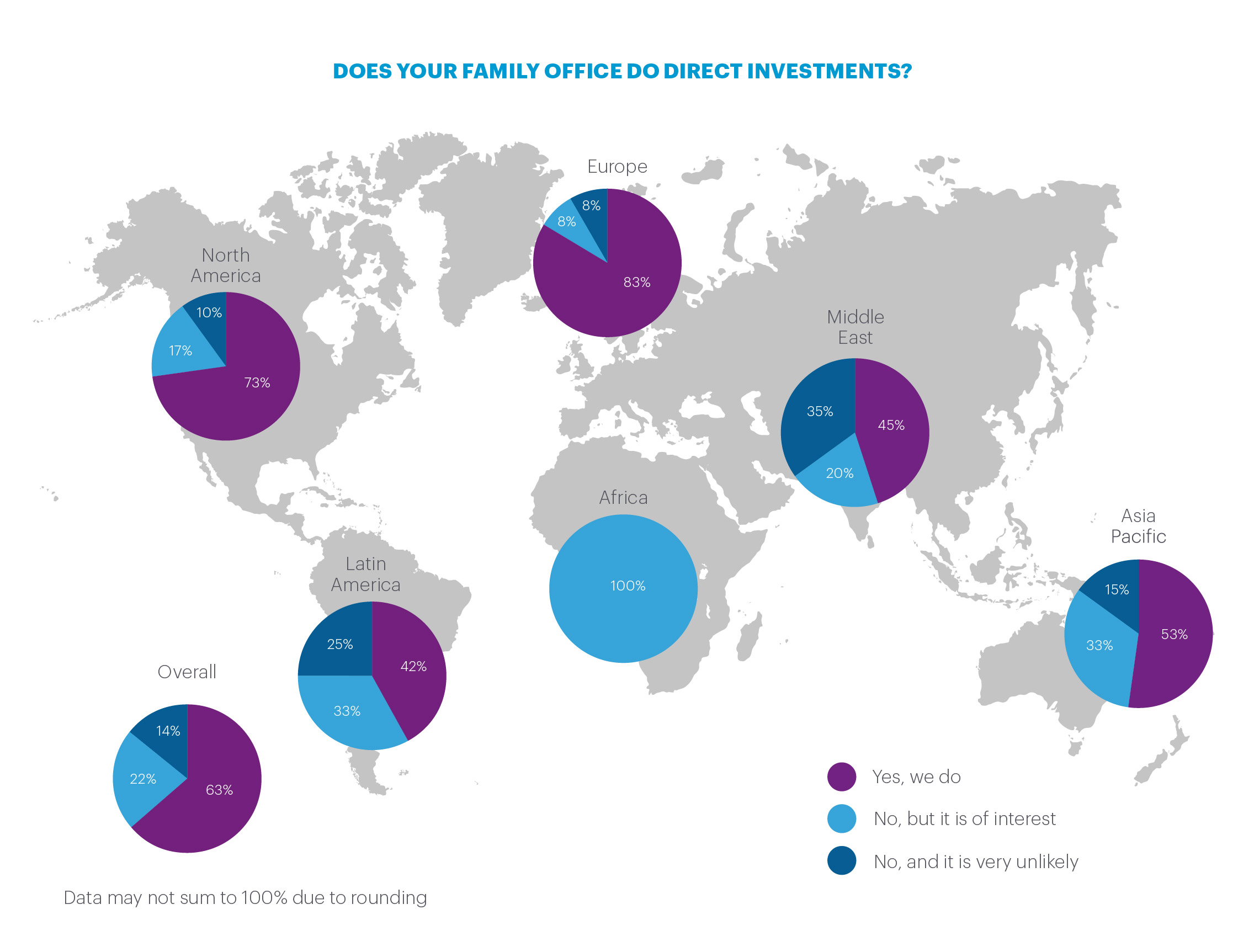

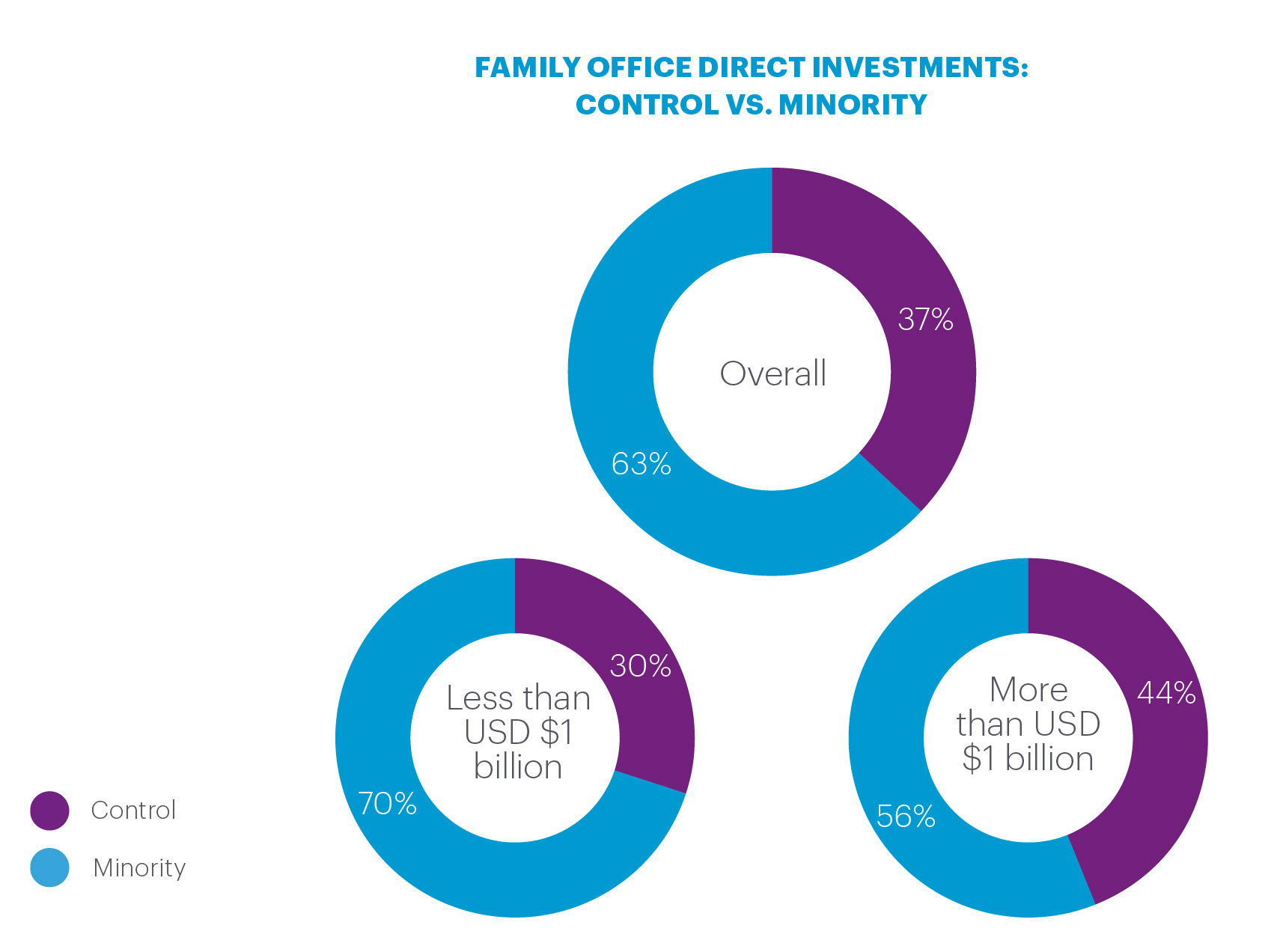

In all, 63% of family offices use direct investments, which as well as investing directly in a business, can mean participating in club deals with other family offices, or directly participating in private equity or venture capital investments. A further 22% of family offices say that they do not currently make direct investments, but it is of interest to them. Size matters here, as larger family offices are more likely to undertake direct investments. For example, among SFOs and FEs, 74% of those with $1 billion or more in assets use direct investments compared to 53% of SFOs and FEs with less than $250 million in assets. In addition, larger family offices have more staff in total and more staff dedicated to private equity and direct investments, giving them more capacity to manage the demands of this asset class.

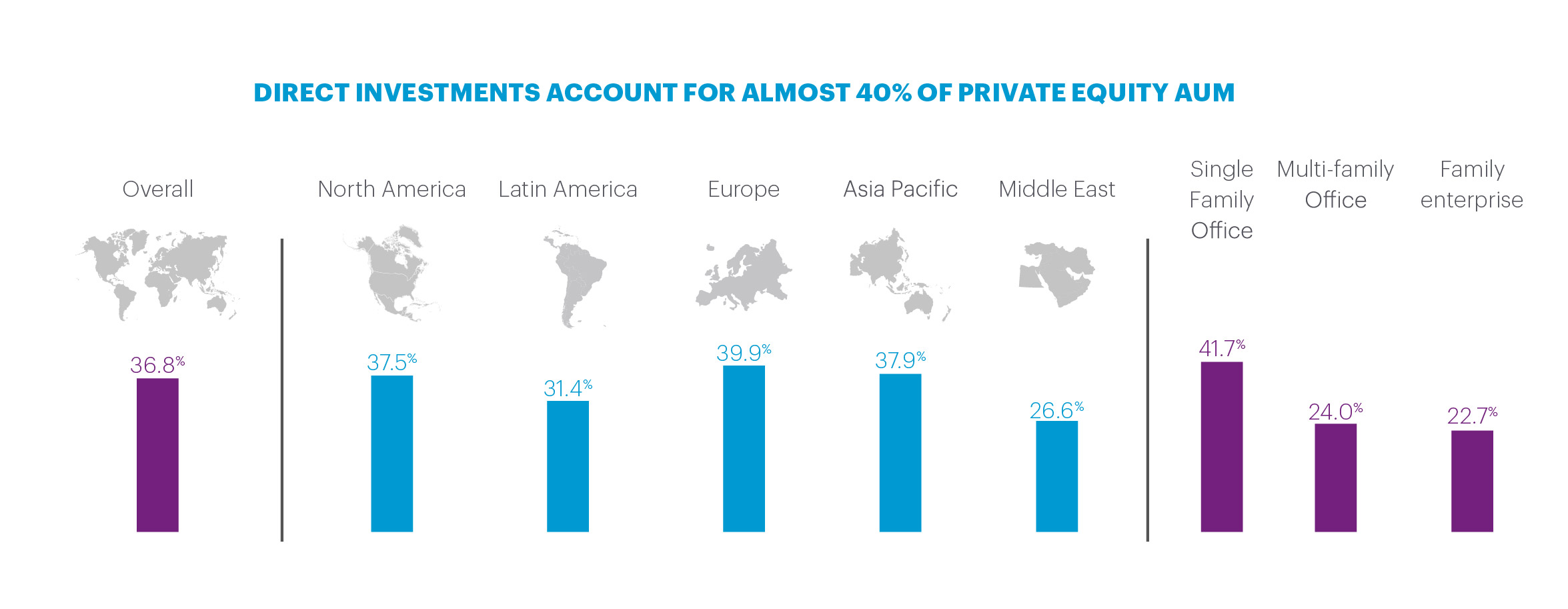

For family offices making direct investments, allocations are often substantial with an average allocation of 37% of private equity assets. This varies from 40% in Europe to 27% in the Middle East. Larger SFOs and FEs tend to have a higher percentage of private equity assets in direct investments (45% for those with $1 billion or more in assets).

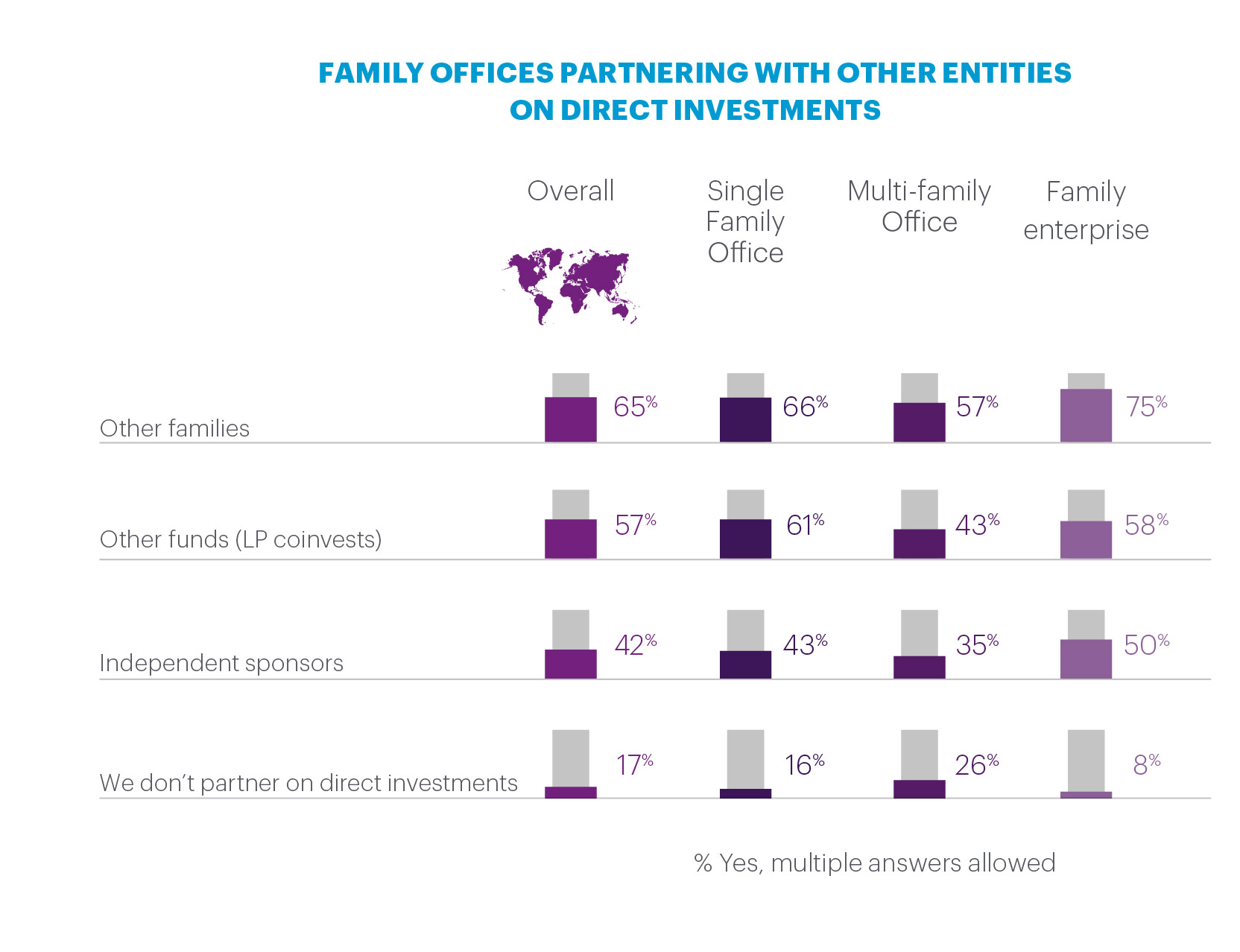

Family offices frequently partner with other entities on direct investments, such as other families, other funds (limited partner, or LP, co-invests) and independent sponsors. By family office type, family enterprises are most likely to partner with other families and independent sponsors, while single family offices show a slightly greater tendency to work with other funds (often through limited partner co-investors or special purpose vehicles).

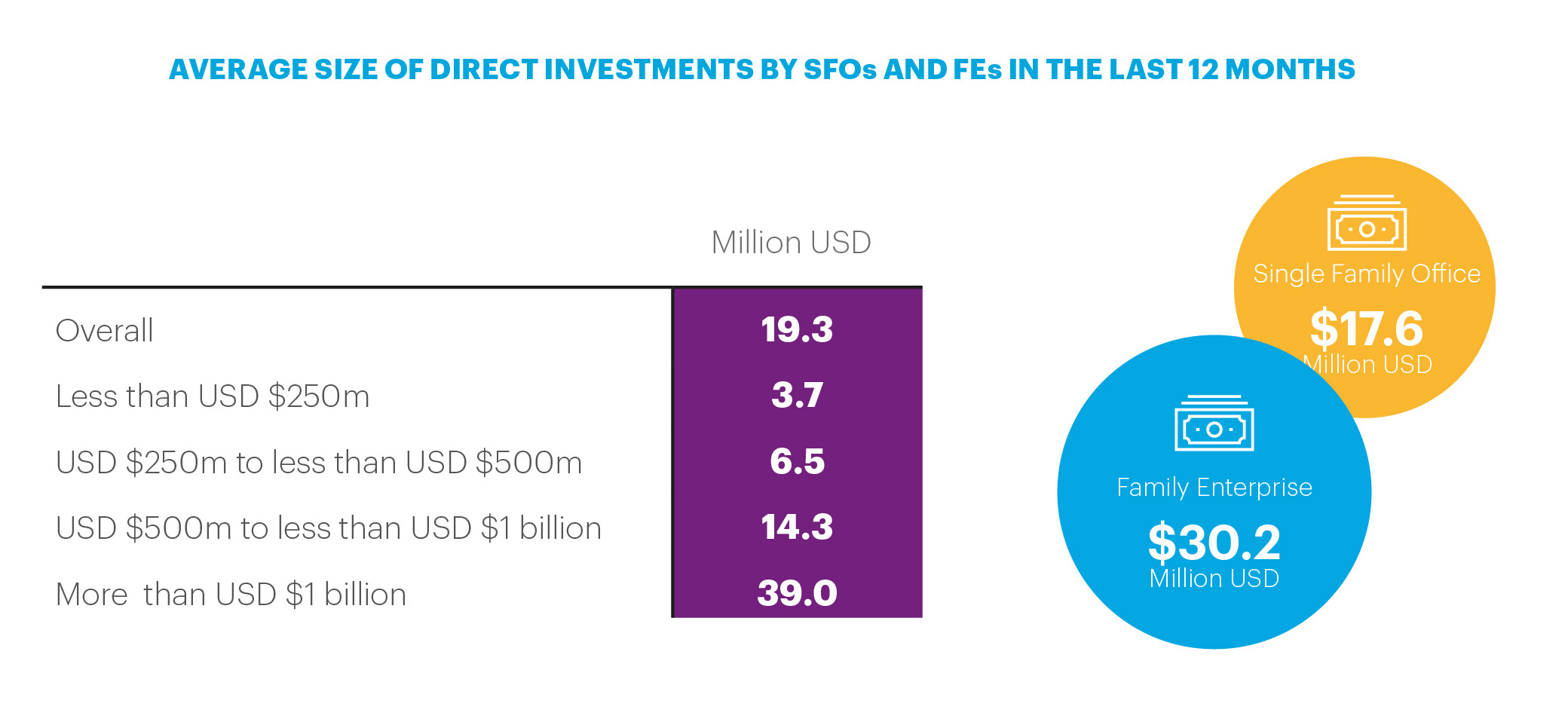

In terms of the size of direct investments, the average investment is $19 million on a global basis, with this increasing with the size of a family office. Family enterprises also make larger direct investments, on average, when compared to single family offices.

One advantage large family offices have with direct investments is that they are more likely to be in a controlling position, or to have influence, allowing more control of exit options and other important aspects of direct investments. For larger family offices with more than $1 billion in AUM, 44% of direct investments have a controlling position, compared to 30% for those with less than $1 billion in assets. By region, European family offices (44%) and North American family offices (42%) were also more likely to have a controlling position in direct investments.

Preferred areas for direct investing

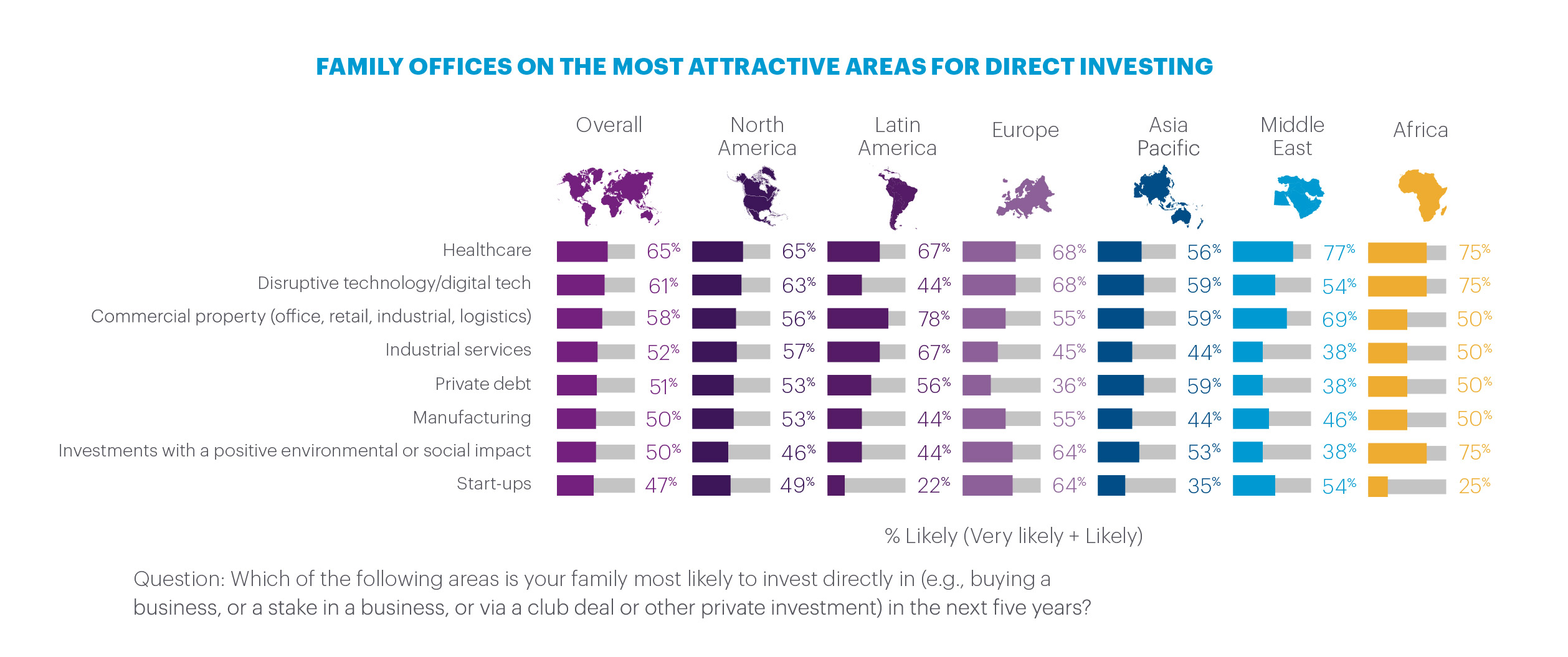

The most popular area for family offices to invest directly in over the next five years is healthcare (65%), followed by disruptive technology and digital tech (61%). Both these areas can offer opportunities to invest in start-ups, and healthcare can encompass areas such as biotechnology, where innovation can drive the development of new therapies and treatments. In addition, both areas may offer investment opportunities at a time when the global economy is struggling.

Healthcare is particularly liked by family offices in the Middle East (77% are likely to invest), while 68% of European family offices are likely to invest in disruptive and digital tech. Over half (58%) of family offices making direct investments plan to invest in commercial property in the next five years and this rises to more than 3 in 4 (78%) in Latin America and to 69% in the Middle East. Commercial property can offer a mix of rental income and capital gains and it can be a relatively stable investment. Against this, events such as the pandemic and the trend to online retail are reducing the investment case for office and retail property for some. Another regional difference is that both investments with a positive environmental or social impact (64%) and start-ups (nearly 64%) are more popular among European investors. Overall, industrial services, private debt, manufacturing and ESG-impactful investments rounded out sectors where a majority of family offices expressed focus.

Family members are often instrumental in deciding on direct investments and their views on the attractiveness of different areas can differ from non-family staff at family offices. For example, family members are more likely to find disruptive technology and digital tech (70% vs. 59%), cryptocurrencies and NFTs (38% vs. 19%), private debt (65% vs. 45%) and residential property (54% vs. 36%) attractive than non-family staff. These results show that family members may have strong views on direct investments and may be more willing to invest in new and developing areas. If this is the case, non-family staff, such as investment managers, may need to support family members by providing quality sourcing, thorough diligence, careful structuring, sound advice and skillful post-close investment management, to ensure that direct investments in what could be high risk, high reward areas are structured and managed in a way that aims to optimize results and limits downside exposure.

The challenges of direct investing for family offices

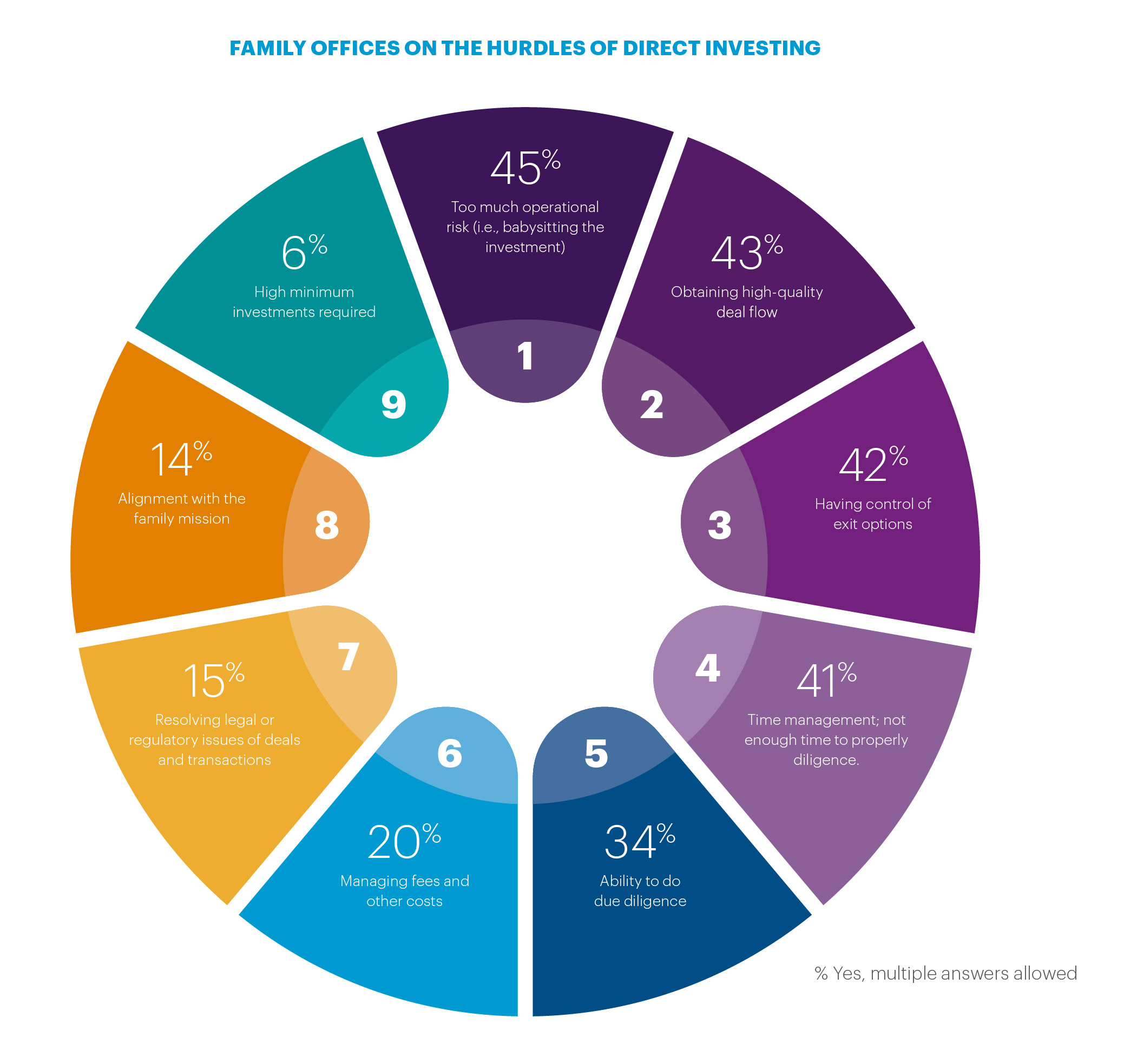

While direct investments can give family offices access to good opportunities and the ability to influence how an investment is managed, they can also be challenging, requiring time and expertise. From identifying suitable opportunities, agreeing to terms, then managing a direct investment through to exit routes and realizing gains, direct investments can be very demanding. For family offices, the biggest challenges of direct investing are taking on too much operational risk (45%), obtaining high-quality deal flow (43%), having control of exit options (42%) and time management issues, including a lack of time for due diligence (41%).

Deal flow was named as the top need for 2023 by family offices

Family office size is an important factor in what they see as the biggest direct investing challenges. Obtaining high-quality deal flow (51%) and having too much operational risk (54%) are more likely to be seen as the biggest challenges at large SFOs and FEs, with over $1 billion in assets. It may be the case that for larger SFOs, deal flow is a critical issue, as more in assets needs to be allocated to suitable opportunities. In contrast, for SFOs and FEs with less than $250 million in assets, having control of exit options is among the biggest challenges (41%), along with managing fees and costs (32%). Small SFOs and FEs are also more likely to find that high-minimum-investment amounts required are a challenge (13% vs. 6% overall).

When asked about the importance of factors behind a decision to make a direct investment rather than use an external fund, family offices recognize the challenges they face. For instance, nearly all (93%) say having the relevant skills and experience in-house is important, and 84% of family offices believe that being able to exit when and how they want is important and consider that when making decisions regarding fund vs. direct investing.

Family offices also see having influence or control (81%) and having influence over the management of a business (78%) as important factors in any decision over investing directly or using a fund, while nearly half (45%) see being able to take a majority stake as being an important factor. Fees and costs are also an important factor when deciding between direct investing and a fund; around two-thirds (67%) see being able to avoid fees as an important factor, while 63% see being able to avoid carried interest as an important factor.

The legal challenges of direct investments

From a legal perspective, the biggest challenges of direct investing are due diligence issues (66%). Structuring investments is also a challenge for 43%, while 40% say that tax and estate planning is a challenge.

Due diligence issues are a particular challenge for family offices in North America (70%) and Asia Pacific (71%), while structuring investments stands out as a challenge in Europe (55%) and the Middle East (54%). Nearly half (46%) of Middle Eastern investors cite regulatory issues as a legal challenge. One possibility is that this is related to the challenges of investing in line with Shariah law for Middle Eastern families.

While there are regional differences on legal challenges, overall, family members (57%) and smaller SFOs and FEs (62% for those with less than $250m) are more likely to see tax and estate planning as a key legal challenge. For the largest SFOs and FEs, with $1 billion or more AUM, over half (51%) put litigation risk as one of the most challenging aspects of direct investing.