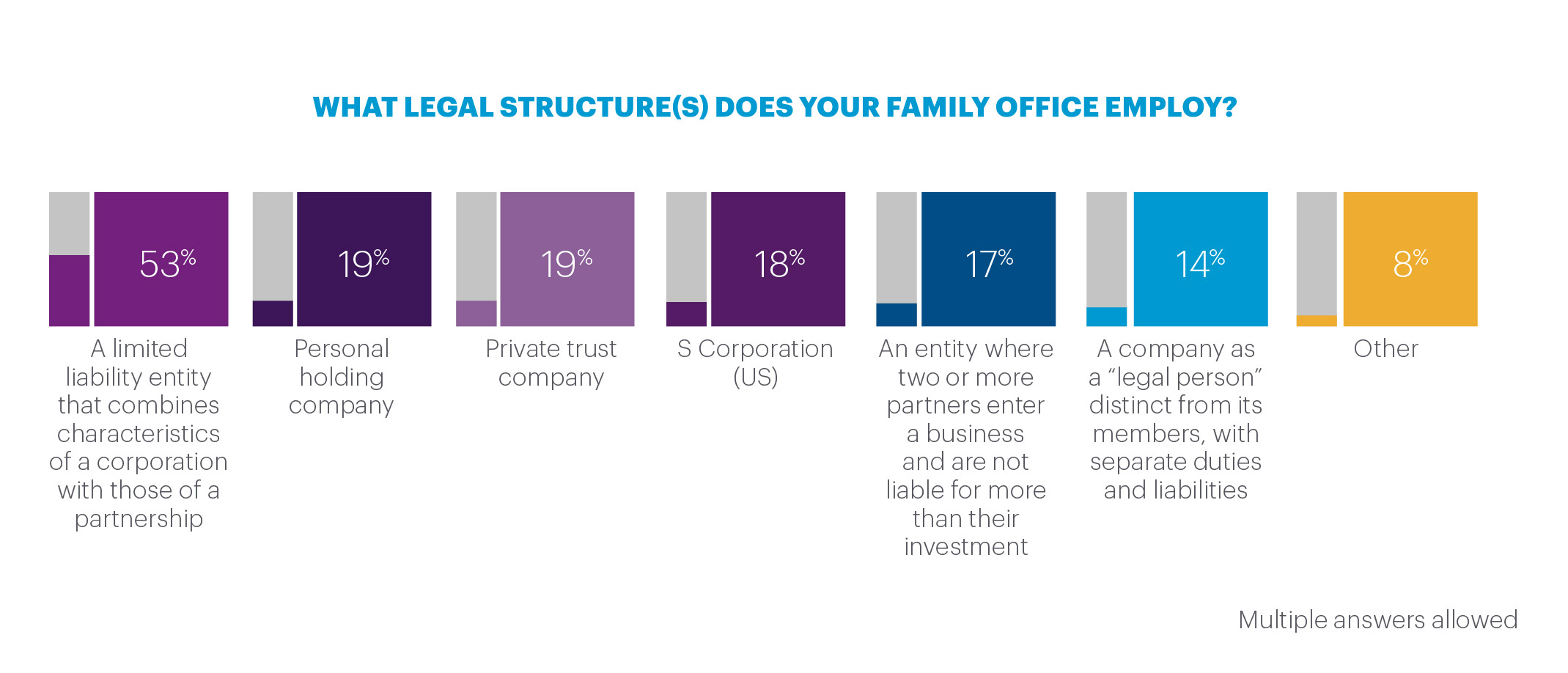

The most common way of structuring a family office is through a limited liability entity that combines characteristics of a corporation with those of a partnership (53%), although a significant number define themselves as a personal holding company (19%) or a private trust company (19%). Limited liability entities are most common in North America (59%), the Middle East (70%) and at the largest SFOs and FEs (62%). The largest SFOs are more likely to be structured as a company (i.e., a separate legal entity from its owners) with the ability to own and transfer property (21%) or as a personal holding company (23).

Almost two-thirds (65%) of family offices have a formal investment policy statement. It is somewhat surprising that many family offices do not have one, as such a document is usually seen as an important foundation for formulating an investment strategy. On the other hand, as key family members can be the main investment decision-makers, they may feel it is unnecessary, or prefer to operate in a nimble manner, without formal guidance.

Regionally, family offices in Europe (58%) and Asia Pacific (60%) are slightly less likely to have a formal investment policy statement, while larger SFOs and FEs are more likely to have a formal investment policy statement; 69% with an AUM over $1 billion compared to 53% with an AUM less than $250 million.

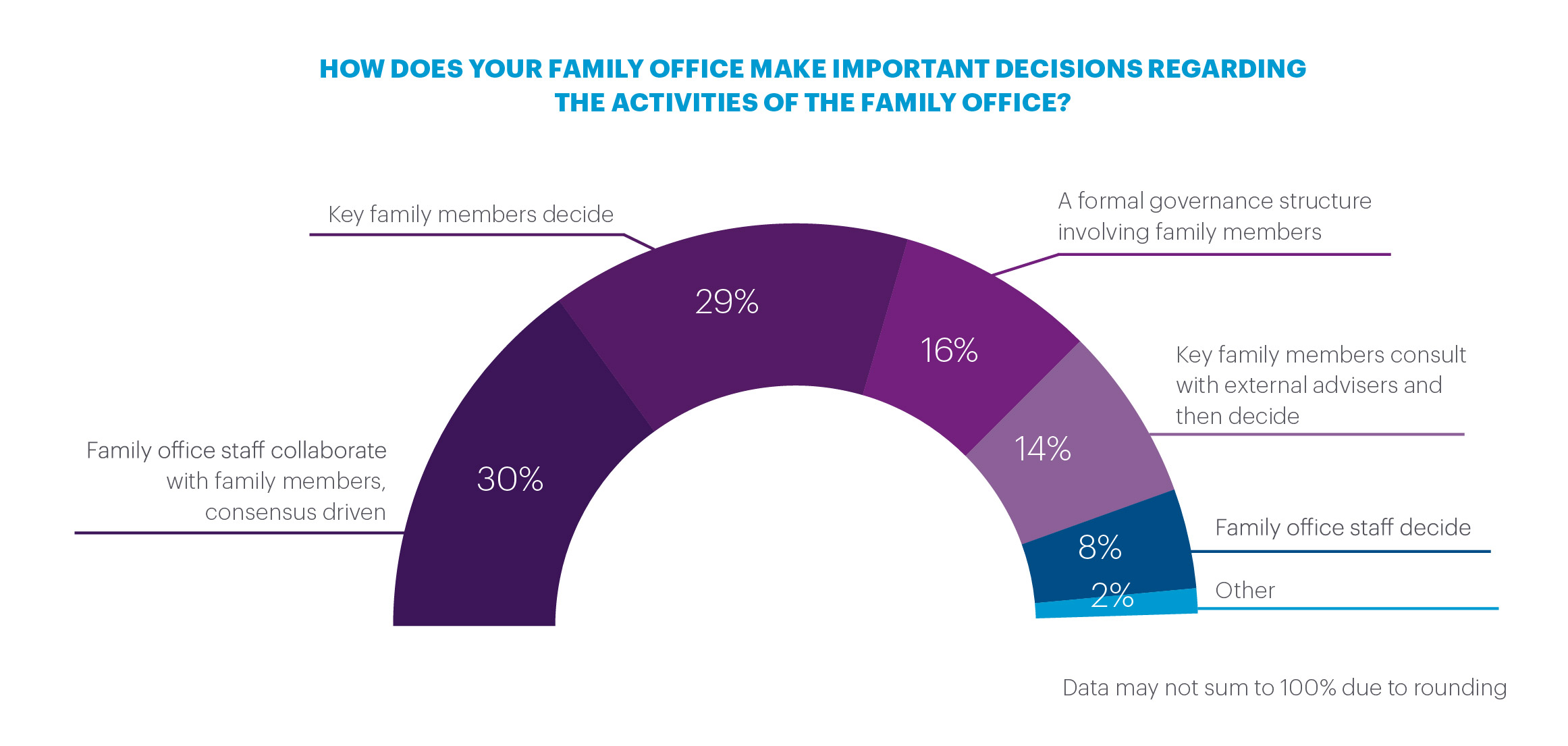

When it comes to investment decision-making, three out of ten family offices (30%) make important investment decisions by family office staff collaborating with family members and then making decisions on a consensus basis, while at 29% of family offices, key family members alone decide.

A collaborative approach between family members and family office staff is more prevalent in North America (35%) and Europe (37%), while key family members deciding is more common in the Middle East (45%) and Latin America (33%).

Important investment decisions are made by key family members at 44% of the smallest SFOs and FEs (under $250 million) but this falls to 19% at SFOs and FEs with over $1 billion in assets. Only 16% of family offices make decisions through a formal governance structure involving family members, but this rises to 40% for the largest SFOs and FEs (over $1 billion in assets).

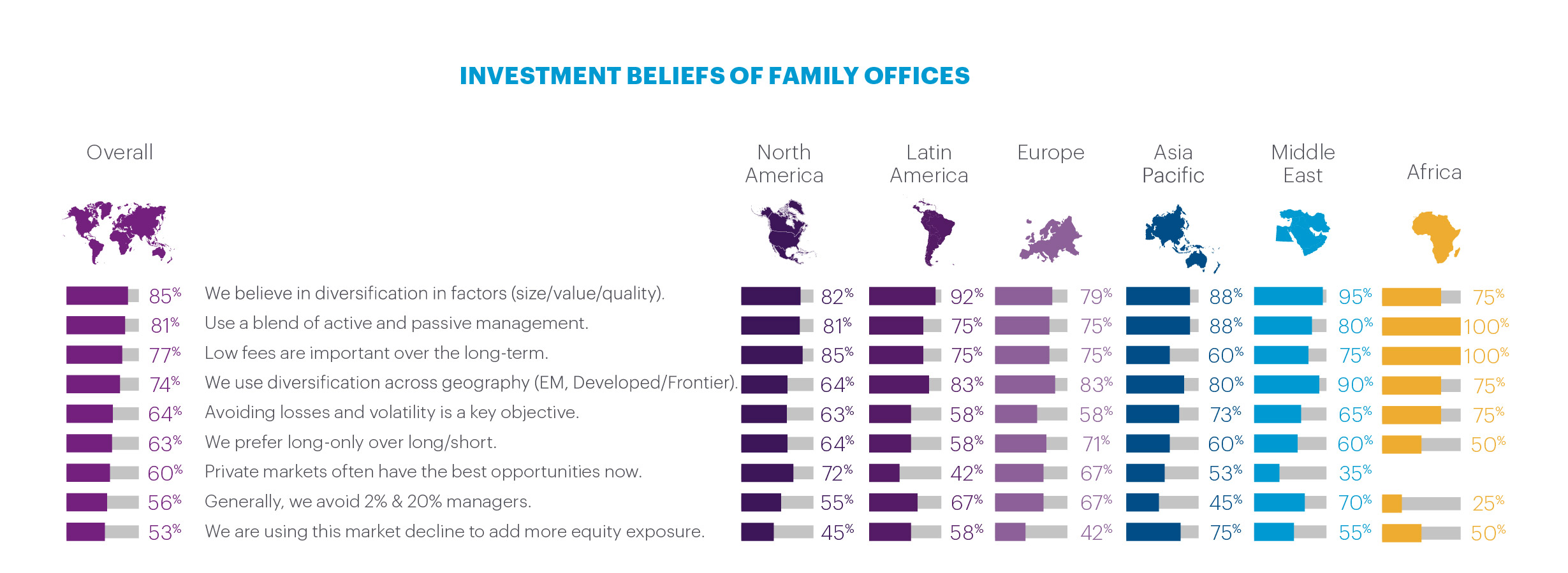

However, when family offices make decisions, diversification is one of their key investment principles, with 85% believing in factor diversification and 74% in geographical diversification. A similar proportion, 81%, believe in using a mix of active and passive management, while slightly less, 77%, believe low fees for the family office are important over the long-term. North American family offices are particularly keen on low fees but are also more likely to believe that private markets have the best opportunities now (72% vs. 60% overall). European family offices are most likely to want to avoid managers applying a “2% & 20%” fee structure, which is the fee structure typically used by hedge funds. For some family offices this may mean looking for discounts on “2% & 20%” fees, others might avoid funds using this type of fee structure entirely. Asia Pacific family offices are most likely to believe in using the market decline to add more equity exposure (75% vs. 53% overall).

Given the important role that family members often have in investment decision-making, it is relevant to look at the views of family members on investment. They are less likely than non-family members or staff to believe in factor diversification (78% vs. 85%) and more likely to believe that private markets often have the best opportunities now (73% vs. 60% overall).

In terms of size, the largest SFOs are less likely to believe that avoiding losses and volatility is a key objective (52% of those with $1 billion or more AUM vs. 69% for those with less than $250 million AUM). Added to this, larger family offices are more likely to share the belief that private markets have the best opportunities now. These differences are predictable to the extent that larger family offices are likely to be better equipped to undertake direct investments and more willing to ride out market volatility in pursuit of growth and returns.

Private equity investing

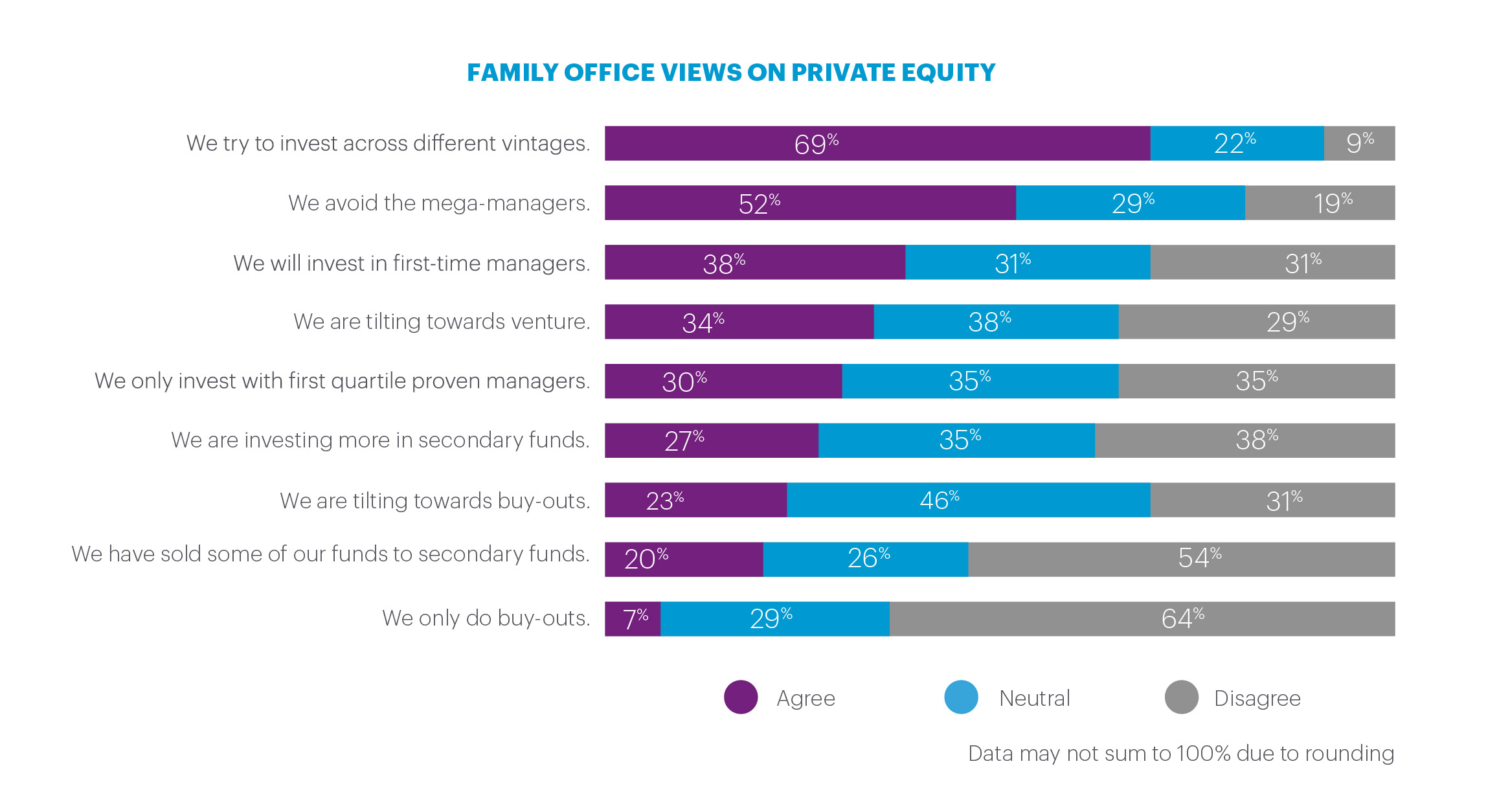

Private equity is an important asset class for many family offices, as it gives access to a wide range of opportunities, from new tech start-ups to major corporate deals backed by private equity funds. From the data, it appears that family offices would prefer to back entrepreneurs with new ideas, rather than benefitting from corporate deal-making, and many (52%) want to avoid the largest private equity managers.

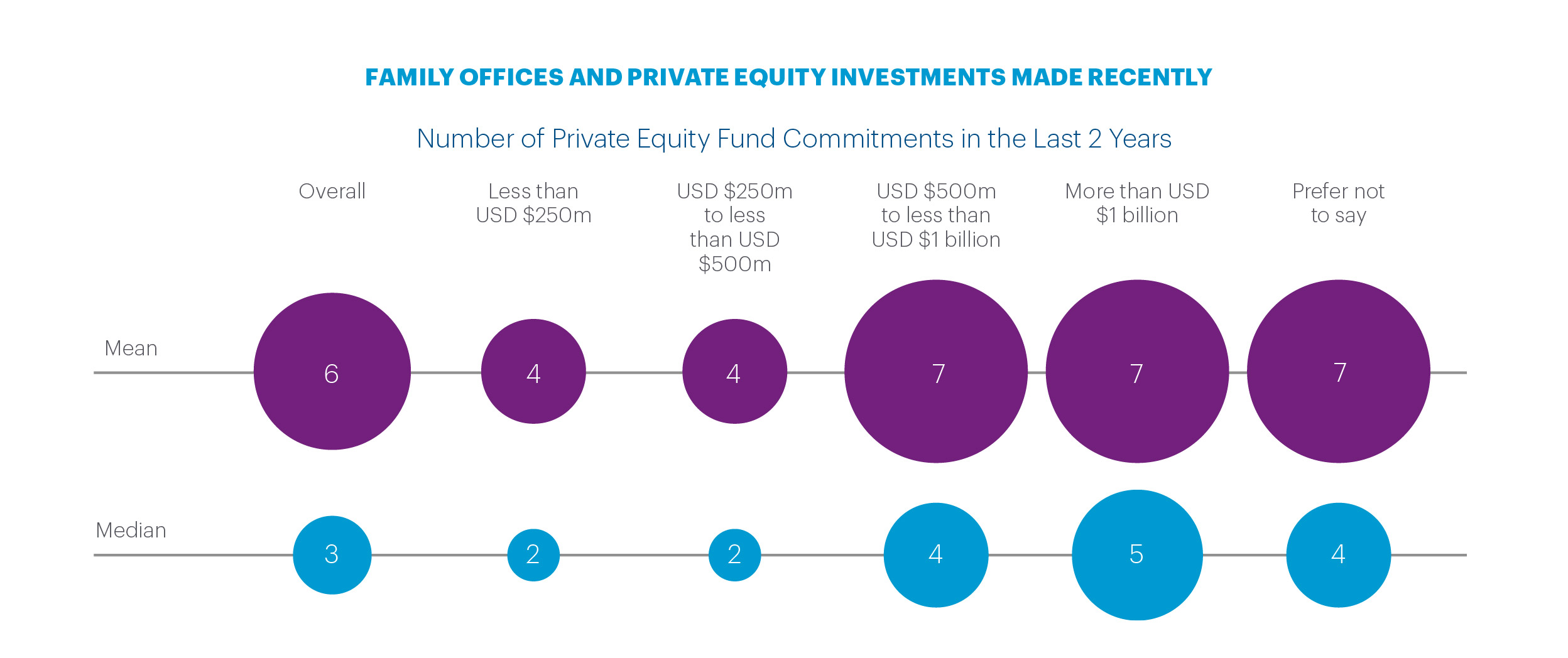

Among SFOs and FEs, the average number of private equity fund commitments made in the last 24 months is 6, with an average of 11 private equity fund managers in each family’s portfolio. Larger SFOs had higher numbers of fund managers (20+) as part of their portfolios. North American family offices have the highest average number of private equity managers in their portfolio, with 16.

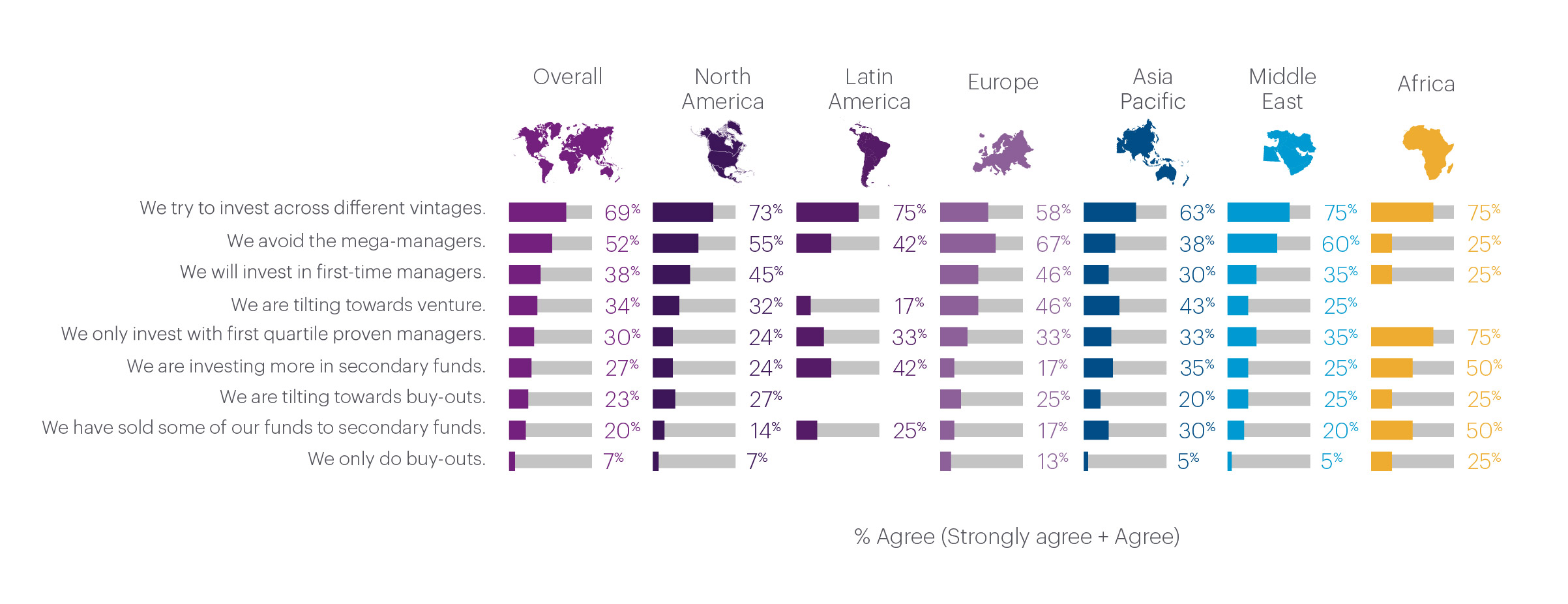

A large majority (69%) of family offices believe in investing across different vintages of private equity, which is important for diversification. This rises to 79% of larger SFOs and FEs, with $1 billion in AUM or more. Larger SFOs and FEs are also more likely to say that they will invest in first-time private equity managers. This may be due to the fact that with larger, diversified allocations to private equity, larger SFOs and FEs can afford to take the risks of first-time managers, who may also be highly motivated and open to lower fees or to negotiate on terms and conditions with investors.

On a regional basis, European family offices are least likely to try to invest across different vintages (58% vs. 69% overall) and most likely to be tilting towards venture (46% vs. 33% overall). European and North American family offices are also most likely to invest in first-time managers, while Asia Pacific family offices are least likely to invest in first-time managers. European investors are also more likely to avoid mega-managers (67% do so vs. 52% overall). Latin American and Middle East family offices are more likely to be investing more in secondary funds (42% and 35% respectively vs. 27% overall).

Compared to non-family office staff, family members are more likely to take a bolder approach to private equity investing. For example, family members are less likely to be tilted toward buy-out, or larger transactions (18% vs. 25% of non-family members) and more likely to be tilting towards venture, or smaller and growing businesses, (40% vs 31% of non-family members). Family members are also more likely to invest in first-time managers (42% vs. 36%).

Overall, these findings on private equity investing show that while family offices want to manage their risks, by diversifying across different vintages, many of them also see it as a source of growth, by investing in first-time managers and by tilting towards venture, avoiding the biggest private equity managers.